ABC Company’s income statement and vertical analysis demonstrate the value of using common-sized financial statements to better understand the composition of a financial statement. A common size statement analysis lists items as a percentage of a common base figure. Creating financial statements in this way can make it much easier when it comes to comparing companies, or even comparing periods for the same company. With regular financial statements, you would have line items listed as their total amounts. When it comes to common size financial statements, each line item gets expressed as a specific percentage of revenue or sales. The balance sheet of a company gives an overview of shareholders’ equity, assets, and liabilities for a reporting period.

- Essentially, it allows data entries to be listed as a percentage of a common base figure.

- When it comes to common size financial statements, each line item gets expressed as a specific percentage of revenue or sales.

- A common-size analysis is unlikely to provide a comprehensive and clear conclusion on a company on its own.

- Much like ratio analysis, vertical analysis allows financial information of a small company to be compared with that of a large company.

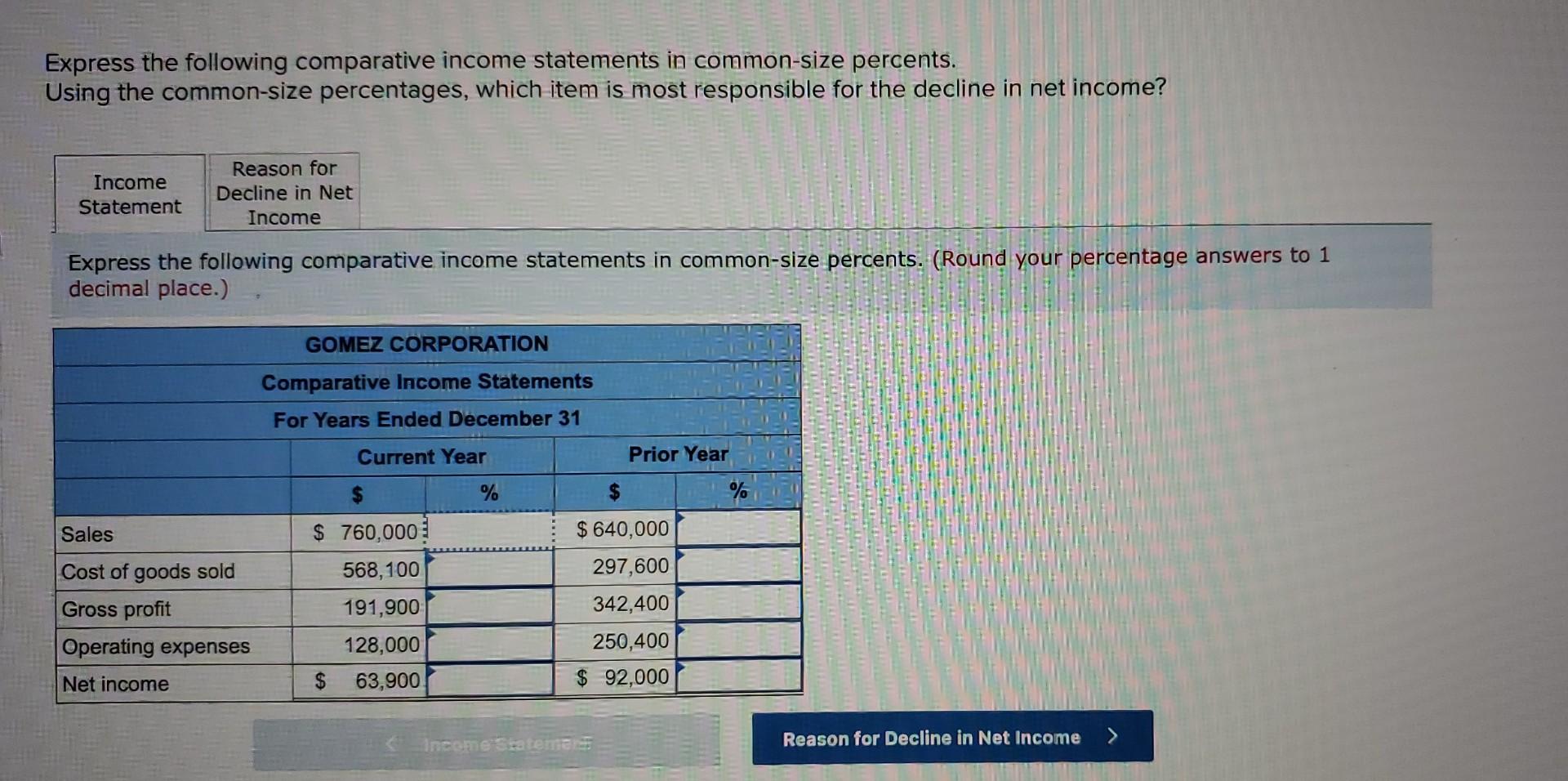

What Is a Common Size Income Statement?

A common size balance sheet analysis gets created with the same rationality as the common size income statement. You can use the balance sheet equation, which express the items in common-size percents. is assets equals liabilities, plus any stockholders equity. Analysts also use vertical analysis of a single financial statement, such as an income statement.

What Is Meant by a Common-Size Balance Sheet?

To prepare a vertical analysis, you select an account of interest (comparable to total revenue) and express other balance sheet accounts as a percentage. On the Clear Lake Sporting Goods’ common-size balance sheet, we see that current assets remained at 80 percent of total assets from the prior to current year (see Figure 5.25). While the balance in the equipment account did change as a percentage of total assets, equipment remained the same at 20 percent. As a result, the financial statement user can more easily compare the financial performance to the company’s peers.

3: Common-Size Financial Statements

It’s worth noting that calculating a company’s margins and the common size calculation are the same. Within each section, there will be additional information that outlines the business activity for each source and use. One of the most common versions of the common size cash flow statement will express any and all line items as a percentage of total cash flow. Each line item on a balance sheet, statement of income, or statement of cash flows is divided by revenue or sales. You might be able to find them on the websites of companies that specialize in financial analysis. By doing this, we’ll build a new income statement that shows each account as a percentage of the sales for that year.

These items are calculated as a percentage of sales so they help indicate how much the company uses them to generate overall revenue. Let’s say that you’re looking into the line items on an income statement for a company. The items include selling and general administrative expenses, taxes, revenue, cost of goods sold, and net income.

Or, they can also help show how each item affects the overall financial position of a company. On this income statement, the common size divides each line item by the total revenue. For example, if the cost of goods sold was $50,000 then you would divide it by $100,000 to equal 50%. A common-size analysis is unlikely to provide a comprehensive and clear conclusion on a company on its own. A short-term drop in profitability could indicate just a speed bump rather than a permanent loss in profit margins. A common-size balance sheet is a comparative analysis of a company’s performance over a time period.

Vertical analysis consists of the study of a single financial statement in which each item is expressed as a percentage of a significant total. Since we use net sales as the base on the income statement, it tells us how every dollar of net sales is spent by the company. For Synotech, Inc., approximately 51 cents of every sales dollar is used by cost of goods sold and 49 cents of every sales dollar is left in gross profit to cover remaining expenses. Of the 49 cents remaining, almost 35 cents is used by operating expenses (selling, general and administrative), 1 cent by other and 2 cents in interest. We earn almost 11 cents of net income before taxes and over 7 cents in net income after taxes on every sales dollar. This is a little easier to understand than the larger numbers showing Synotech earned $762 million dollars.

To conduct a vertical analysis of balance sheet, the total of assets and the total of liabilities and stockholders’ equity are generally used as base figures. All individual assets (or groups of assets if condensed form balance sheet is used) are shown as a percentage of total assets. Performing common-size calculations for several different time periods and looking for trends can be especially useful.