A company’s cash flow statement breaks down all of the uses and sources of its cash. For example, it could be cash flows from financing, cash flows from operations, and cash flows from investing. Horizontal analysis relates to specific line items and then compares them to a similar item that was included express the items in common-size percents. in the previous financial period. Vertical analysis relates to analyzing specific line items against the base item, and this is from the same financial period. Before breaking down the different types of common size analysis, it’s worth understanding that it can be conducted in two ways.

Common-Size Assets and Common-Size Liabilities and Equity

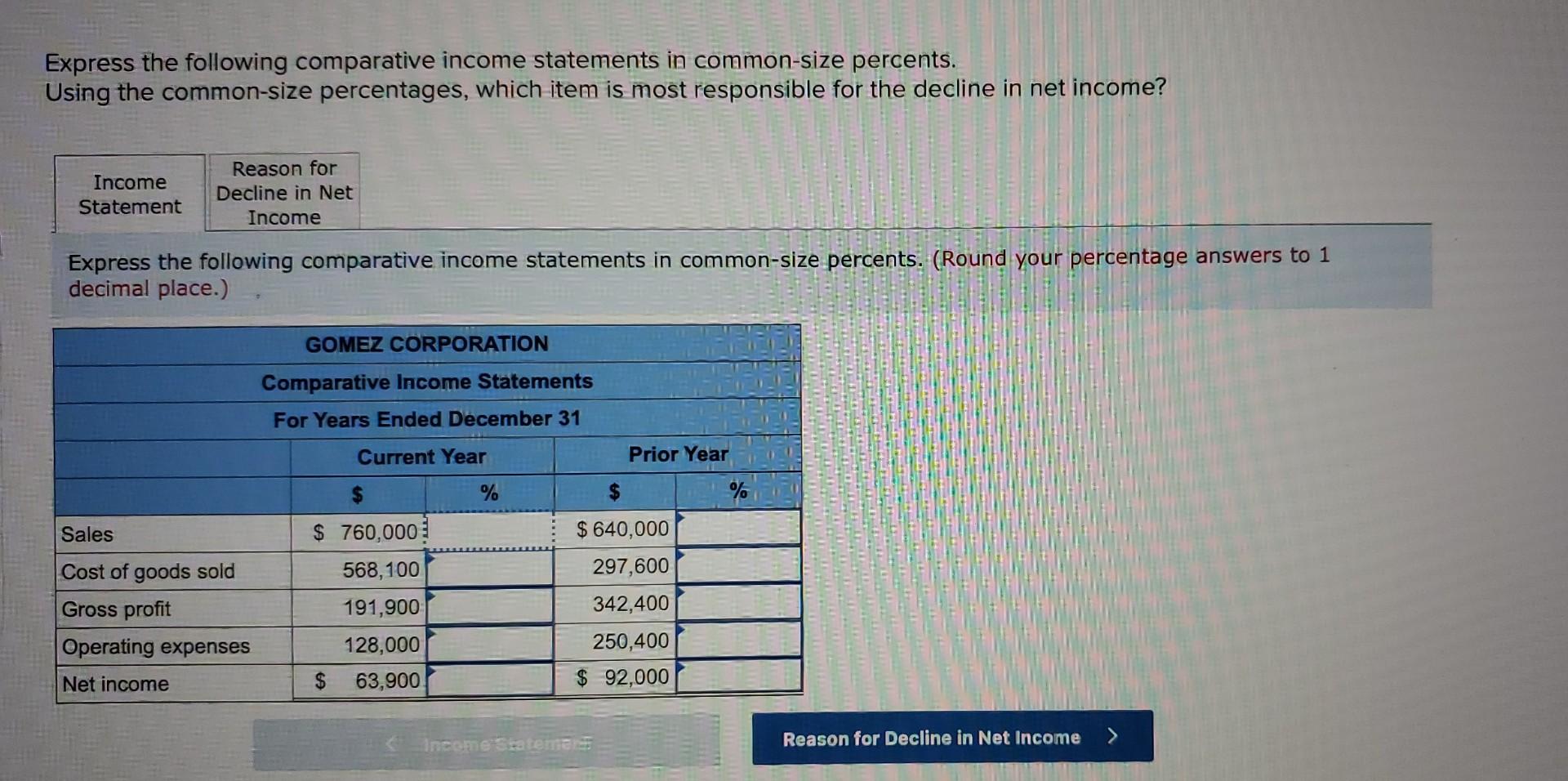

A common size income statement is an income statement in which each line item is expressed as a percentage of the value of revenue or sales. It is used for vertical analysis, in which each line item in a financial statement is represented as a percentage of a base figure within the statement. Consists of the study of a single financial statement in which each item is expressed as a percentage of a significant total. Vertical analysis is especially helpful in analyzing income statement data such as the percentage of cost of goods sold to sales. Where horizontal analysis looked at one account at a time, vertical analysis will look at one YEAR at a time.

3: Common-Size Analysis of Financial Statements

- The common-size balance sheet functions much like the common-size income statement.

- They can also look at the percentage for each expense over time to see if they are spending more or less on certain areas of the business, such as research and development.

- For Synotech, Inc., approximately 51 cents of every sales dollar is used by cost of goods sold and 49 cents of every sales dollar is left in gross profit to cover remaining expenses.

- While the balance in the equipment account did change as a percentage of total assets, equipment remained the same at 20 percent.

To calculate net income, you subtract the cost of goods sold, selling and general administrative expenses, and taxes from total revenue. After some calculations, you determine the revenue for the company to be $100,000. It can also highlight the expense items that provide a company a competitive advantage over another.

Common-Size Income Statements

For example, a company might choose to gain more market share by sacrificing operating margins. Also known as the profit and loss statement, the income statement is an overview. To find net income using the income statement equation, you simply minus sales from expenses. One company may be willing to sacrifice margins for market share, which would tend to make overall sales larger at the expense of gross, operating, or net profit margins. The cash flow statement in terms of total sales indicates that it generated an impressive level of operating cash flow, averaging 26.9% of sales over three years. It’s important to add short-term and long-term debt together and compare this amount to the total cash on hand in the current assets section.

Notice that Clear Lake spends 50 percent of its sales on cost of goods sold while Charlie spends 59 percent. Common size financial statement analysis can also be applied to the balance sheet and the statement of cash flows. Using common size percentages allows you to gain a different perspective of each line item.

On the income statement, analysts can see how much of sales revenue is spent on each type of expense. They can see this breakdown for each firm and compare how different firms function in terms of expenses, proportionally. They can also look at the percentage for each expense over time to see if they are spending more or less on certain areas of the business, such as research and development. On the balance sheet, analysts commonly look to see the percentage of debt and equity to determine capital structure. They can also quickly see the percentage of current versus noncurrent assets and liabilities. The common-size percentages on the balance sheet explain how our assets are allocated OR how much of every dollar in assets we owe to others (liabilities) and to owners (equity).

Creating common-size financial statements makes it easier to analyze a company over time and compare it to its peers. Using common-size financial statements helps spot trends that a raw financial statement may not uncover. The common size version of this income statement divides each line item by revenue, or $100,000.

Financial statements in dollar amounts can easily be converted to common-size statements using a spreadsheet. Share repurchase activity as a percentage of total sales in each of the three years was minimal or non-existent. Now that you have covered the basic financial statements and a little bit about how they are used, where do we find them? In this next section we will explore the requirements for what needs to be reported, when, and to whom. This would come at the expense of good profit margins but would increase revenues. The key benefit of a common-size analysis is that it allows for a vertical analysis by line item over a single period, such as quarterly or annually.

Cash is listed as an individual entry in the assets section with the total balance being listed on the left and its percentage of total assets being listed on the right. The income statement also uses this presentation with revenue entries referencing total revenues and expense entries referencing total expenses. The common size percentages can be subsequently compared to those of competitors to determine how the company is performing relative to the industry. For Example, Company A has $10 million in total assets, $7 million in total liabilities and $3 million in total equity. As the common-size balance-sheet reports the assets first in the order of liquidity, the top entry would be of Cash worth $2 million.

Essentially, it helps evaluate financial statements by expressing the line items as a percentage of the amount. It helps break down the impact that each item on the financial statement has, as well as its overall contribution. The common-size method is appealing for research-intensive companies because they tend to focus on research and development (R&D) and what it represents as a percent of total sales. The common-size strategy from a balance sheet perspective lends insight into a firm’s capital structure and how it compares to its rivals. You can also look to determine an optimal capital structure for a given industry and compare it to the firm being analyzed.

By analyzing how a company’s financial results have changed over time, common size financial statements help investors spot trends that a standard financial statement may not uncover. The common size percentages help to highlight any consistency in the numbers over time–whether those trends are positive or negative. Common-size financial statements facilitate the analysis of financial performance by converting each element of the statements to a percentage.